Wisdom Teeth and Interest Rates

Wisdom Teeth and Interest Rates

How a lower neutral rate of interest is hurting my post-surgery recovery.

After years of delay and procrastination, I finally completed my wisdom teeth extraction last week.

Going into the procedure, I was very skeptical of the timing of the procedure. In my head, wisdom teeth extractions are associated with unnecessary prescriptions for opioids, varying recovery times, and swollen faces that resemble chipmunks. By scheduling the procedure within four days of my orientation date for my summer job, I knew I was playing a dangerous game.

Now that the game has begun, I thought I would document some of my thoughts to distract myself from any minor pain I may be experiencing during the recovery period.

During the hours following the procedure, it is recommended that you take Tylenol and Ibuprofen, ice the sides of your face for the first 24 hours, and place gauze pads in the locations where the teeth were extracted to help the blood clot faster.

The recommendation I was most concerned about was icing the sides of my face. The problem was that my mouth, which was still numb from the local anesthesia given to me during my procedure, was not letting me communicate properly. And what I very much wanted to communicate to the people around me was the details about materials I would need to make a DIY ice pack: socks, a safety pin, and ice.

After two failed attempts at replicating the DIY ice pack described above, I settled on a different solution: holding each ice pack with each hand to each side of my face — which inadvertently took away my dexterity.

I couldn’t use my hands and I couldn’t speak, leaving me nothing to do except think. And at that time, I was thinking about the worthiness of manually icing my face and its striking similarities to a fundamental problem in macroeconomics.

One of the most effective ways to prevent me from looking like a chipmunk during my orientation day was to ice my face. Icing my face would only be effective if done within the initial 24-hour period, even though swelling would occur 2-3 days after the procedure. As a result, I had to sacrifice my dexterity now so that I could avoid looking like a chipmunk later. This made icing my face a cruel tradeoff. And my willingness to make the tradeoff was interest.

I have proudly been comparing my existence to an economy for a long time now. I observed how my psychological well-being mirrored the “business cycle,” where within the path of long-run output (personal development), there would be downturns and upswings. Certain activities that I enjoy such as playing basketball would perform the function of expansionary policy that closes output gaps.

But now, “my inner economy” was experiencing a unique crisis that couldn’t be solved by playing basketball, requiring me to come up with a new metaphor.

Interest is a Tradeoff

For many, interest is the lever that the Federal Reserve controls, which sends stock prices upwards, downwards, and sideways. But what interest more broadly represents is the tradeoff between spending later and spending now. For those who choose to spend later, interest is a reward for sacrificing enjoyment now for enjoyment later. For those who spend now, interest is a cost — either from the value that is lost from foregoing the opportunity to spend later or the literal cost of living beyond your means.

A theoretical example demonstrating this tradeoff is someone who borrows money from a friend and pays interest. The interest payment is the reward for the friend who sacrifices the ability to spend now and loans his money. Conversely, the interest payment is the borrower’s cost of having to spend now beyond their means. If interest rates are high, the reward for the friend who lends money is higher. If interest rates are low, then the reward for the friend is lower and the costs for the borrower are lower.

Now if interest rates are low, one might think there won’t be enough friends who are willing to loan money if there is so little reward. Thankfully, we have commercial banks that can create money from thin air. With the power of creating money, interest becomes a tradeoff that is exploited to earn profit.

Interest from assets that a bank holds such as loans handed out, minus the interest on liabilities that a bank owes such as savings accounts, comprises the profitability of a commercial bank. It’s why the interest earned from depositing money in a savings account at a bank is typically much lower than the interest charged for borrowing money from the bank. In most advanced economies, there is a central bank that controls a headline interest rate, which provides strategic guidance for interest rates across loans and savings accounts across the economy.

My inner economy does not have a central bank because I generally assume little to no centralized control over the events that occur in my life. But interest rates still exist without central banks and in my current situation, there is a behavioral interest rate that is influencing whether or not I transact the long-term investment of icing my face.

Central bankers and economists are obsessed with chasing this abstract, mythical, godlike value called r-star, or the neutral rate of interest. Based on the dynamics of the economy, there is a neutral rate of interest that reflects the participants of an economy’s willingness to sacrifice spending now for spending later. Or more precisely, the average reward that participants receive for their sacrifice.

In every economy, there is an r-star value affected by productivity growth, savings rates, asset markets, inflation expectations, treasury bond yields, and a bazillion other factors. Like the unemployment rate and inflation metrics, r-star is a characteristic of an economy that fluctuates frequently. But unlike the unemployment rate and inflation metrics, r-star is impossible to exactly calculate.

If my inner economy’s r-star is higher, then I am more willing to invest in reducing the future swelling of my face, even with the costs, such as my dexterity, that are incurred. I might believe the reward for my sacrifice to be greater than if my r-star was lower.

From the self-observed empirical evidence, however, it was blatant that my inner economy’s r-star that day was low. My back was killing me from holding up the ice pack to my face and my clothes were becoming wet because the ice would start melting thanks to my consistently delayed replacement of the ice. And if r-star truly reflects the more structural dynamics of an economy, then my r-star has been declining for years.

Since college has started, a deep-rooted, structural impatience has spread throughout my inner economy that has increased my indifference towards making tradeoffs that may benefit my future.

Already, I experience body pains now because of my long-standing intolerance for stretching before exercise. Reading a book is nearly impossible for me because of my insistence that New York Times and Wall Street Journal articles would sustain my ability to attentively read things. I experience hair loss that I could have easily made preventative measures towards, starting my path toward joining the rest of the bald men in my family — a future that I have been warned of since infancy.

I have refused to make many long-term investments and to think I will start now by icing my face would be ridiculous.

In other words, my r-star level is quite low because of many possible but ultimately unprovable reasons. Much like the U.S. economy.

R-star’s Relevance to Recession-Fighting

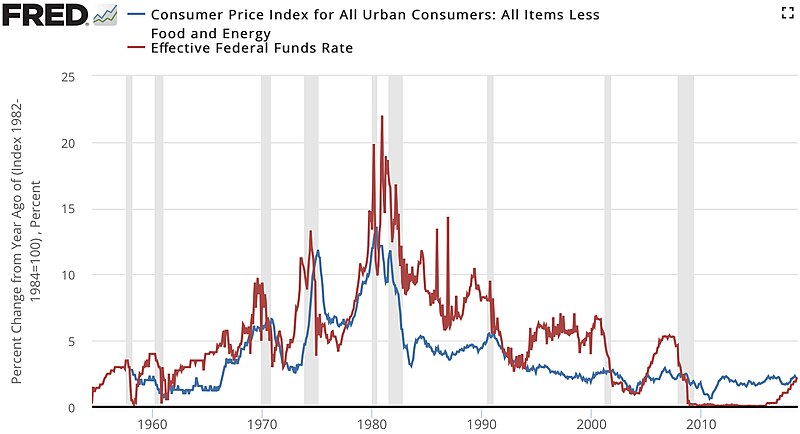

A lot of the novice commentary about inflation and the Federal Reserve that I often hear concerns how interest rates have been too low for too long. In the late 70s and 80s, the Federal Reserve notoriously hiked interest rates to double digits. Now, it is a big deal for the Federal Reserve to increase interest rates above just 1 percent. R-star is central to understanding why the Federal Reserve has behaved this way.

The perceived level of r-star is one of the most important of the many variables that dictate how central banks set monetary policy. If the economy is in decline, then central banks will set interest rates below r-star to encourage economic expansion, by rewarding spending in the present rather than in the future. In an inflationary economic environment created by excessive expansion, interest rates will be set above r-star to contract the economy, consequently increasing the reward for spending in the future rather than in the present.

Remember that r-star signifies the “neutral rate of interest.” If the Federal Reserve decided to set interest rates at the current r-star, then theoretically the economy would not expand or contract from its current state. But this would be very hard because determining r-star, in practice, is more of an art than a science.

Despite central bankers’ difficulty estimating r-star, it is clear as day that r-star has fallen. Even with near-zero interest rates, monetary policy was not expansionary enough to even create 2 percent GDP growth during the 2010s. In the 1970s, on the other hand, 3 percent interest rates proved to be expansionary enough to enable double-digit inflation.

{kind=link}

By viewing monetary policy through the lens of r-star, many economists conclude by induction that the inefficacy of near-zero interest rates to promote economic expansion is the most concrete evidence of historically low levels of r-star. Comparatively, the litmus test for analyzing my inner economy’s levels of r-star is my willingness to ice my face after having my wisdom teeth yanked out of my mouth.

Coming up with a phenomenon in my inner economy that is analogous to how monetary policy works would be like pulling a rabbit out of my ass. It wouldn’t be real and if it was it would stink. I won’t try to make the case that based on my understanding of my internal r-star, I can actively push all “interest rates” relevant to all personal situations upwards by taking a 30-minute hot shower.

Once you understand r-star and its relevance to monetary policy, theories explaining why there are low r-star levels such as the “global savings glut” and “secular stagnation” can be comprehensible. The methodology behind Federal Reserve interest rate decisions can be understood to be more complex than just guessing a number. Tracing the effects and the efficacy of interest rate decisions, which we are frighteningly uncertain about, becomes more fascinating.

Along with a better understanding of macroeconomic events, however, comes paranoia of potential macroeconomic problems. Demographic trends such as our aging population become much scarier. Growing inequality seems like even more of an unstoppable problem. Sometimes I will feel that even the most incremental progress made through policy change, is contingent on the policy’s design striking an impossible balance that cannot deter the economy’s path towards economic growth. It is truly as if the further down the rabbit hole I get, the closer I am to realizing that my head is up my own ass.

The difficulty of writing about a sprawling subject such as interest rates is that I don’t quite know what I don’t know and what I definitively do know is only the tip of the iceberg. Comparing myself to an economy and configuring metaphors equating the willingness to ice my face after dental surgery to interest rates are exercises that verify to me that I do understand some things. It also demonstrates that I am more willing to write 2000 words about r-star in the most labyrinthine manner possible instead of icing the sides of my face.